From Empty Nest to Full House… Multigenerational Families Are Back!

Multigenerational homes are coming back in a big way! In the 1950s, about 21%, or 32.2 million Americans shared a roof with their grown children or parents. According to a recent Pew Research Center report, the number of multigenerational homes dropped to as low as 12% in 1980 but has shot back up to 19%, roughly 60.6 million people, as recently as 2014.

Multigenerational households typically occur when adult children (over the age of 25) either choose to, or need to, remain living in their parent’s home, and then have children of their own. These households also occur when grandparents join their adult children and grandchildren in their home.

According to the National Association of Realtors’ (NAR) 2016 Profile of Home Buyers and Sellers, 11% of home buyers purchased multigenerational homes last year. The top 3 reasons for purchasing this type of home were:

- To take care of aging parents (19%)

- Cost savings (18%, up from 15% last year)

- Children over the age of 18 moving back home (14%, up from 11% last year)

Donna Butts, Executive Director of Generations United, points out that,

“As the face of America is changing, so are family structures. It shouldn’t be a taboo or looked down upon if grown children are living with their families or older adults are living with their grown children.”

For a long time, nuclear families (a couple and their dependent children) became the accepted norm, but John Graham, co-author of “Together Again: A Creative Guide to Successful Multigenerational Living,” says, “We’re getting back to the way human beings have always lived in – extended families.”

This shift can be attributed to several social changes over the decades. Growing racial and ethnic diversity in the U.S. population helps explain some of the rise in multigenerational living. The Asian and Hispanic populations are more likely to live in multigenerational family households and these two groups are growing rapidly.

Additionally, women are a bit more likely to live in multigenerational conditions than are their male counterparts (20% vs. 18%, respectively). Last but not least, basic economics.

Carmen Multhauf, co-author of the book “Generational Housing: Myth or Mastery for Real Estate,” brings to light the fact that rents and home prices have been skyrocketing in recent years. She says that, “The younger generations have not been able to save,” and often struggle to get good-paying jobs.

Bottom Line

Multigenerational households are making a comeback. While it is a shift from the more common nuclear home, these households might be the answer that many families are looking for as home prices continue to rise in response to a lack of housing inventory.

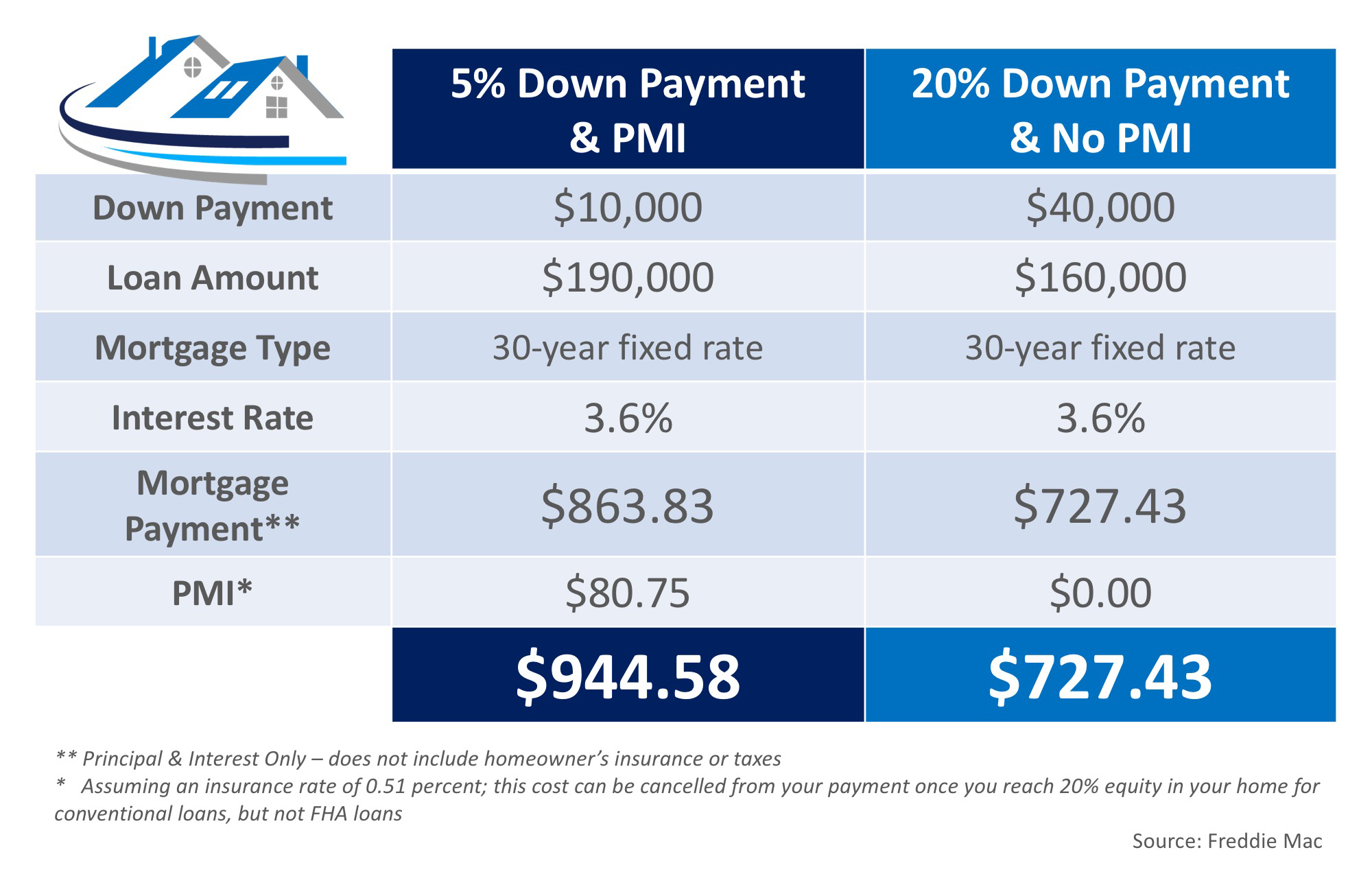

When it comes to buying a home, whether it is your first time or your fifth, it is always important to know all the facts. With the large number of mortgage programs available that allow buyers to purchase a home with a down payment below 20%, you can never have Too Much Information (TMI) about Private Mortgage Insurance (PMI).

When it comes to buying a home, whether it is your first time or your fifth, it is always important to know all the facts. With the large number of mortgage programs available that allow buyers to purchase a home with a down payment below 20%, you can never have Too Much Information (TMI) about Private Mortgage Insurance (PMI).

There are many people sitting on the sidelines trying to decide if they should purchase a home or sign a rental lease. Some might wonder if it makes sense to purchase a house before they are married and have a family. Others may think they are too young. And still, others might think their current income would never enable them to qualify for a mortgage.

There are many people sitting on the sidelines trying to decide if they should purchase a home or sign a rental lease. Some might wonder if it makes sense to purchase a house before they are married and have a family. Others may think they are too young. And still, others might think their current income would never enable them to qualify for a mortgage.

![Buying a Home Can Be Scary... Know the Facts [INFOGRAPHIC] | MyKCM](../../../../kcmmedia/2016/10/24133924/20161028-ENG-STM-1046x667.jpg)

![Do You Know the Cost of Renting vs. Buying? [INFOGRAPHIC] | Simplifying The Market](../../../../wp-content/uploads/2016/10/20161014-Rent-vs.-Buy-STM.jpg)

![Mortgage Rates by Decade Compared to Today [INFOGRAPHIC] | Simplifying The Market](../../../../wp-content/uploads/2016/10/20161007-Mortgage-Rates-STM.jpg)