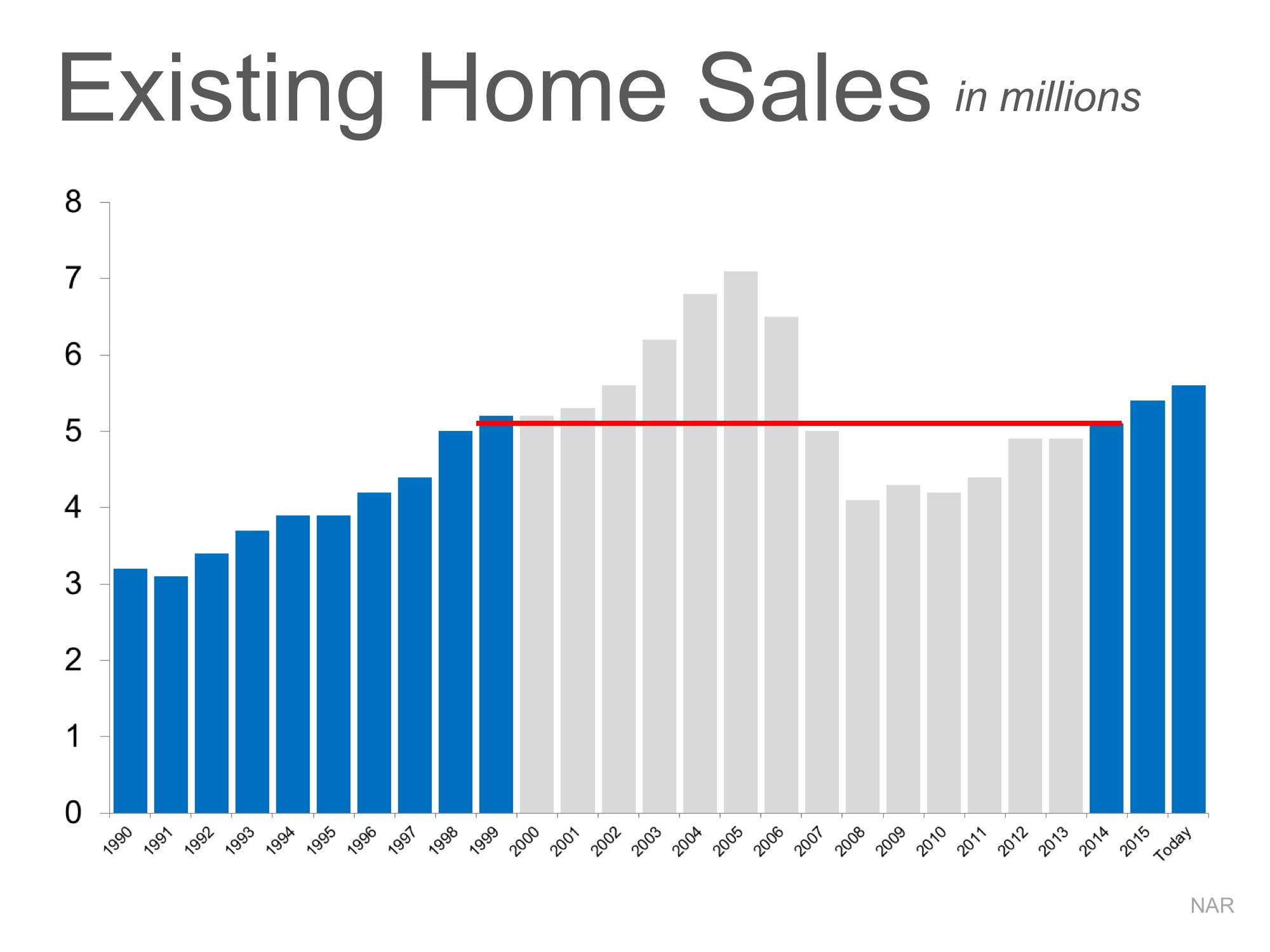

Mortgage Standards Easing TOO MUCH? NO!!

There is no doubt that getting a mortgage is easier today than it was right after the housing crash a decade ago. However, the easing of credit availability has led to some questioning of whether or not we are headed for another housing crisis.

Let’s put everything into the proper perspective.

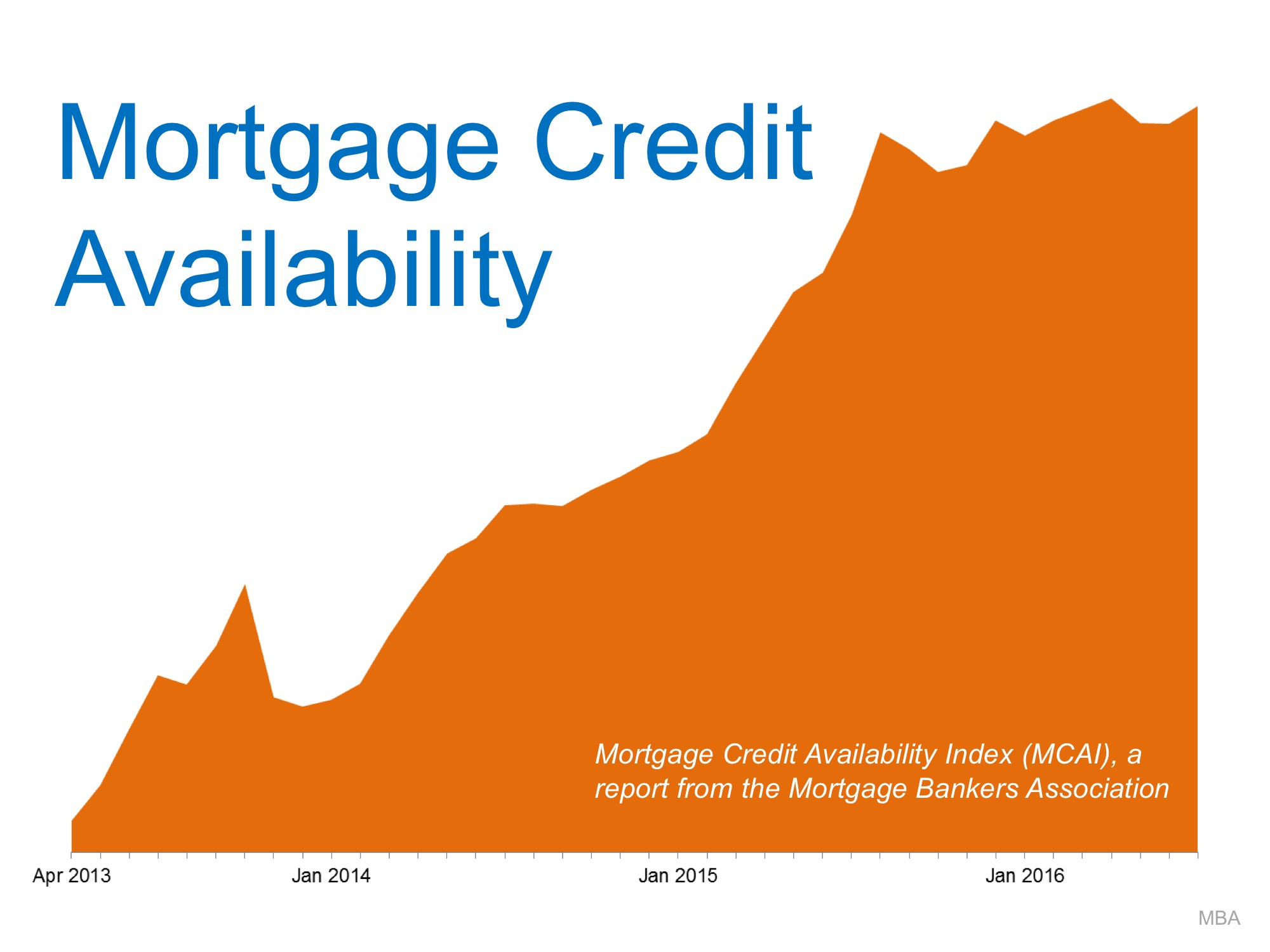

Mortgage Credit Availability Over the Last Three Years

Getting a home mortgage has definitely gotten easier over the last three years as evidenced by theMortgage Credit Availability Index, issued by the Mortgage Bankers Association, in the following graph (the higher the index, the easier it is to get a mortgage):

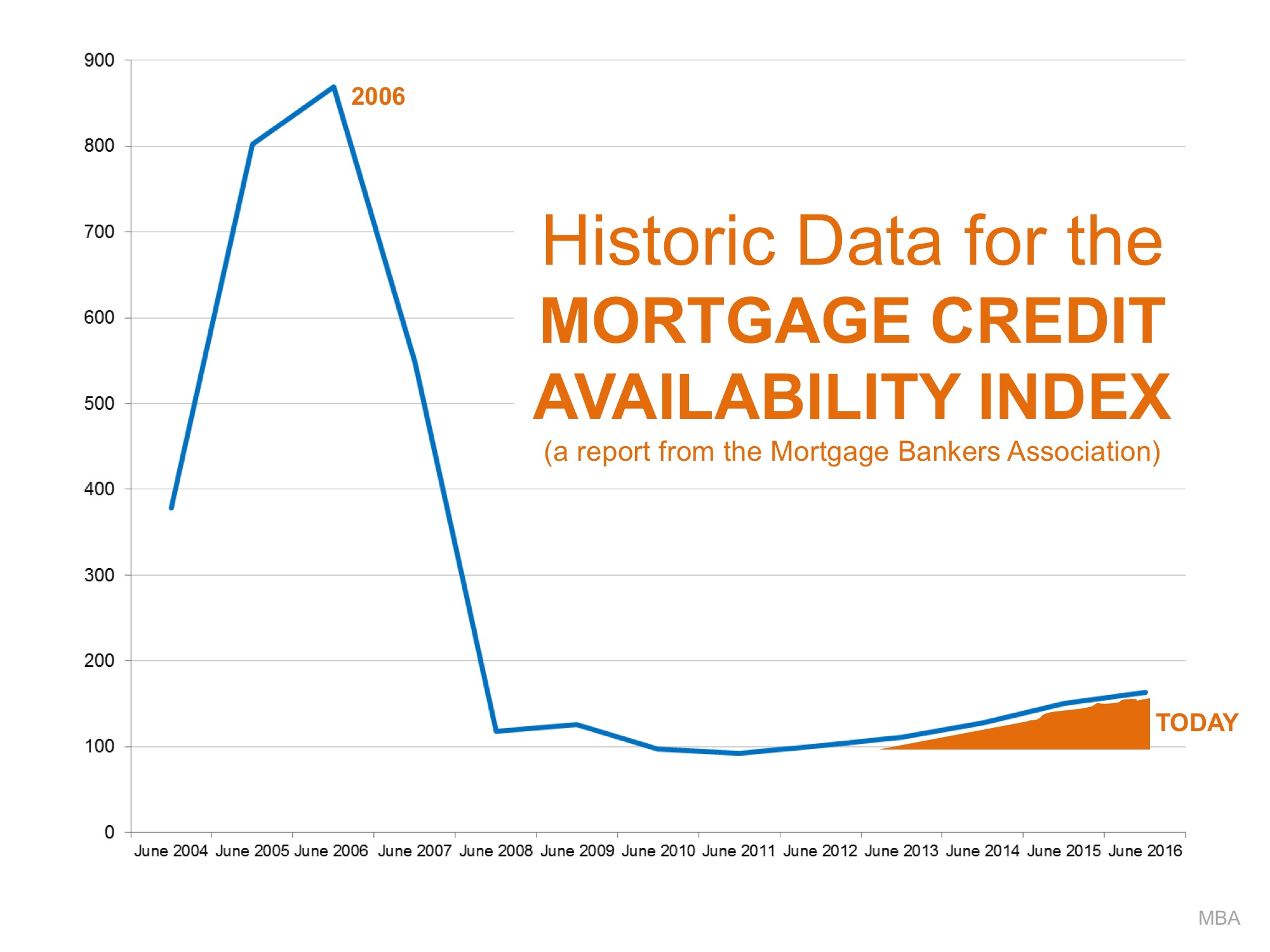

However, if we look further back at the index we see quite a different story.

Mortgage Credit Availability Today Compared to 2006

The graph below shows the index going back to 2004, and the first graph we showed you above is represented by the small, orange, triangular section all the way in the lower-right corner.

As this visual easily illustrates, today’s index is nowhere near the levels it shot up to in 2006.

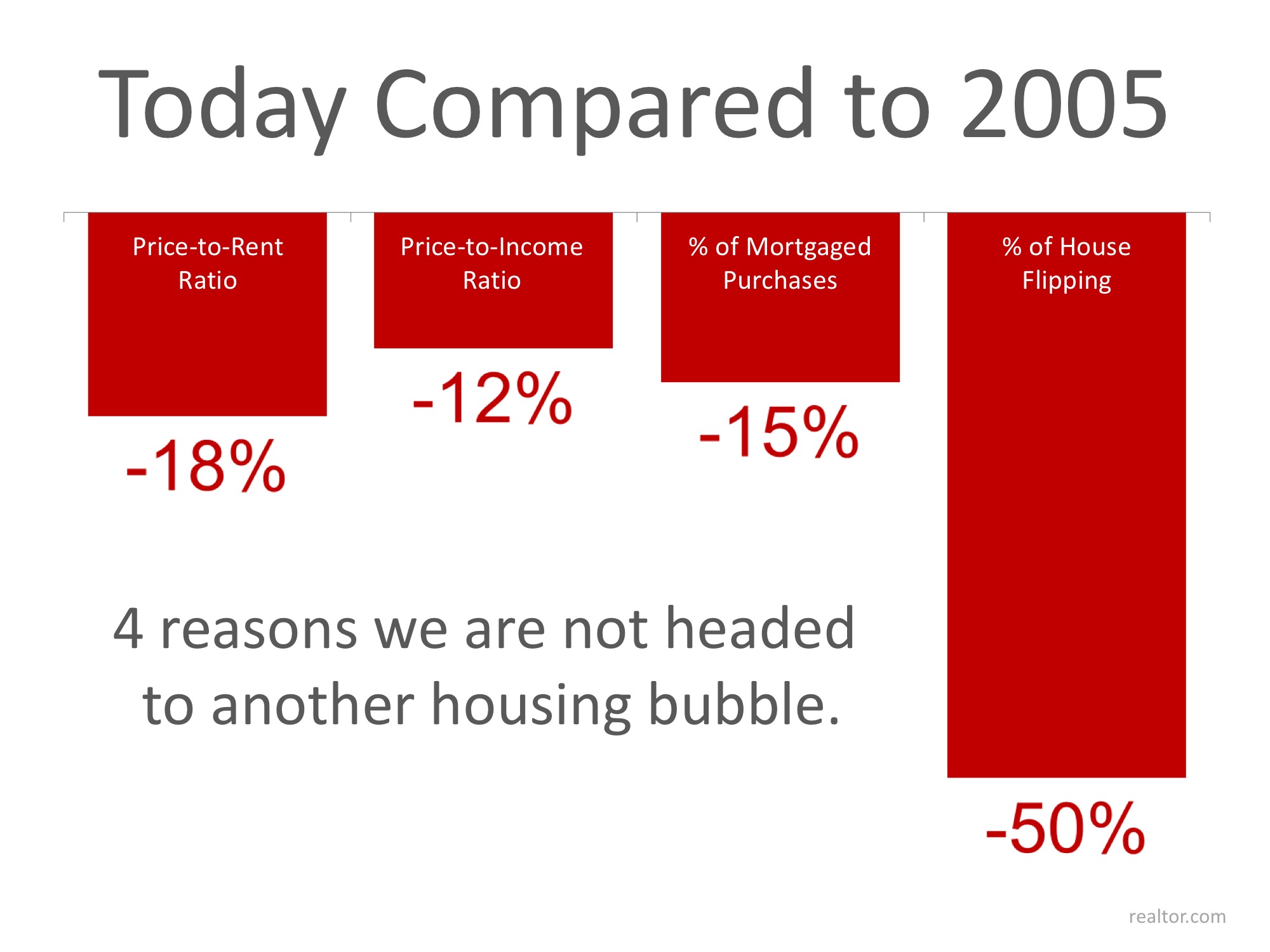

Bottom Line

Mortgage credit is definitely easing. However, we are not coming close to the lax standards that caused the housing crisis of last decade.

![Home Prices Up 5.61% Across The Country! [INFOGRAPHIC] | Simplifying The Market](https://www.simplifyingthemarket.com/wp-content/uploads/2016/09/20160909-STM-ENG.jpg?a=294801-4dd7a167b497c72694456006a520f3f4)

![Sales at Highest Pace in 9 Years [INFOGRAPHIC] | Simplifying The Market](https://www.simplifyingthemarket.com/wp-content/uploads/2016/06/Sales-Highest-in-9-Years-STM-.jpg?a=294801-4dd7a167b497c72694456006a520f3f4)

![‘Old Millennials’ Are Diving Head-First into Homeownership [INFOGRAPHIC] | Simplifying The Market](https://www.simplifyingthemarket.com/wp-content/uploads/2016/08/Old-Millennials-ENG-STM.jpg?a=294801-4dd7a167b497c72694456006a520f3f4)